The 4% Rule: How Fast Can You Retire?

What is your "Financial Freedom Number"?

In this blog, I’ll discuss:

The famous “4% rule” for retirement or financial freedom

The relationship between your investing rate and how fast you can retire

Some real numbers behind reaching financial freedom in 10 years

Extra resources if you’d like to learn more

What is the 4% Rule?

The 4% rule is a guideline used to determine how much you need for retirement. It assumes you can safely withdraw 4% of your total retirement savings in your first year of retirement:

4% × total savings = annual spending

Thus, 1/25 of total savings = annual spending

Therefore, reworking this equation:

Total retirement savings = annual spending × 25

In simple terms:

If you build up an investment portfolio large enough to allow a 4% annual withdrawal -and you can live off that 4% - you’re considered financially free.

The idea is that your portfolio should be invested in a way that its real growth (after inflation) exceeds 4% annually. This way, you won’t erode your capital over time. Your portfolio grows (via capital gains and dividends), and you only withdraw 4%, leaving the rest to compound.

👉 I’ll be hosting a free online Investing Masterclass focused on Financial Freedom - sign up here

The flip side of the 4% rule is that you need 25× your annual living costs to reach financial freedom. This is your “financial freedom number.”

Example:

If your living costs are $5k monthly (or R100k*), your annual costs are $60k (R1.2 million). Your financial freedom number would then be $1.5 million (R30 million).

👉 You can use my Financial Freedom Calculator to calculate your number.

Of course, this is a simplified rule, and there are some valid criticisms of the rule. I would most importantly highlight:

Your investment fund has to be invested in order to achieve sufficient growth to maintain a minimum 4% real returns. So you cannot just have all of your savings lying in cash or low-risk, low-yielding assets.

If you live in a country where inflation could run high in the future, it could completely derail your retirement plans. It is safer to be conservative and have more in your fund (like 30 times your annual living costs).

If you’re going to receive a pension or social security in retirement, you only need to save for what you expect to spend “above” what you’ll be receiving.

How Fast Can You Reach It?

The chart below illustrates how your savings rate affects how quickly you can retire:

A 15% savings rate typically means 40 working years

A 30% savings rate shortens that by 10+ years

An extreme 66% savings rate could help you reach financial freedom in just 10 years

A 10-Year Path to Financial Freedom?

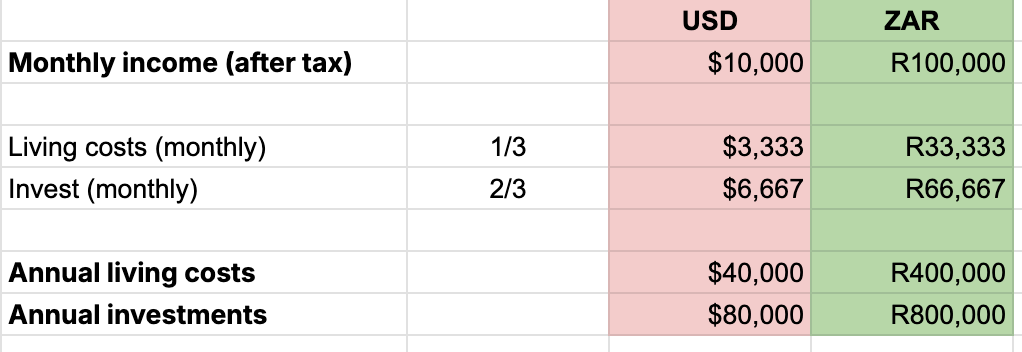

Let’s explore what it might look like to actually achieve financial freedom in 10 years.

Let’s look at two scenarios: Someone earning $10k/month (after tax) and someone earning R100k/month (after tax). To reach financial freedom in 10 years, it would mean investing 2/3 of post-tax income, therefore living off 1/3:

Assuming a reasonable average return (see my YouTube video for more detail), and you invest two-thirds of your income:

After 10 years, your portfolio could be worth $1.1 million or R14 million (these are assumptions, not guarantees)

Here’s the trick: If you’re investing ⅔ of your income, that means you’re living on only ⅓. That’s a lifestyle well below your means - and it needs to stay that way even after reaching your financial freedom number.

You can’t suddenly start “living it up” once you hit the number because higher spending could cause your investments to run dry prematurely.

How Much Will You Be Able to Spend?

At the 10-year mark:

A 4% annual withdrawal from your portfolio would allow for:

Withdrawals of $47k/year or R575k/year, respectively

After accounting for capital gains tax, your annual spending amount might be:

$44k/year or R529k/year

Now compare this to your current living costs adjusted for 10 years of inflation:

This gives a replacement rate of:

82% (USD) and 73% (ZAR)

What Does a Replacement Rate of 82% Mean?

It means you'll be able to spend 82% of your current lifestyle (adjusted for inflation) in 10 years.

So you'd need to make some cuts to maintain the 4% withdrawal rate—unless you boost your income or savings now. Considering in this scenario you’re already only living off 1/3 of your income - making further cuts might not be realistic.

We can’t guarantee outcomes, but I can tell you fairly confidently that you are not going to achieve financial freedom by just holding your cash in a savings account. After you’ve paid tax on the interest earned, the returns hardly keep up with inflation.

I think it’s never been more important to bring diversification into your portfolio, global diversification to get exposure to strong currencies, countries, and industries. It’s also crucial to scrutinize your portfolio for investment fees because just a 1% fee could cut your retirement values by 20%!

As you know by now, I am very interested in the psychology of money. Toward the end of Sunday’s YouTube video, I discuss my personal views of extremely frugal living to reach financial freedom in 10 years. I think work gives purpose. Reaching financial freedom could give you the peace of mind to change jobs or start a business - but I cannot imagine what I’d do with myself if I had to “retire” in 10 years’ time. Reaching financial freedom is a balance between making sacrifices now, for future financial freedom - but I don’t think it should be at the end of not enjoying life for 10 years because you’re chasing a number. This becomes living a “deferred life plan” but watch my YouTube video from 11:00 onwards if you’re interested in this 2-minute discussion :)

Learn more:

Use my financial freedom calculator to calculate your number!

Paid subscribers also get my calculations, more details in this blog

Watch my YouTube video on this topic

Sign up for my free online Masterclass on 26 April here

I’m attending my high school reunion in Bloemfontein on 16 May and hosting a Money With Carla workshop there: Join us!

*For simplicity's sake, I assumed a USD/ZAR exchange rate of R20.

Disclaimer: None of my content is personal financial or tax advice, it is for educational purposes only. Always do your own research or speak to an adviser before making any investment decisions.

Hi Carla I certainly like the work you are doing unfortunately this type of advice was not around in my twenties the done thing was invest in RA's and company pensions. I am now 60 and in the last 5 years I have been seriously looking at my retirement funding which despite never withdrawing any of my provident funds when changing jobs I find my savings are inadequate. If I dont seriously save in the next 5 years I would have to work much longer. There are a few mistakes I made. In my 20-40 I only invested in company provident funds and often with very conservative portfolio risk as most funds through companies have fixed options that cater for everyone. In my 40s I started investing in property as the leverage made sense by using the banks money to fund property. I invested a Million in a Holiday rental home in Mozambique which has created positive cash flows that were used to fund shortfalls in other 2 bed townhouses in SA. I have 7 of the properties today and most of them will be fully paid in the next 5 years before retirement. For 10 years I almost stopped investing in provident funds as I became self-employed in a company where I could dictate my rules for retirement funding. During those 10 years i invested only R3000 per month on retirement believing my property portfolio would bring in the balance of retirement funds. Unfortunately, through conservative influences and people like Harry Dent predicting a major financial collapse my investments were in stable funds not yielding high returns. Also in the stage of life 40 to 50 there are many expenses unique to parents in SA that is private schooling and university which prevent you from having significant funds for retirement savings. Now I am in a position where I have to save 35 to 40% of my gross income in RA's to get close to my financial goals for retirement. I invest in RA's for the tax saving as I can reduce my income in retirement and draw additional income in my wife's name through the property investments in the trust thus reducing income tax. I am in the 45% tax bracket so every cent I invest in RA is funded by tax deductions of 45% up to the R350k limit. In addition, both my wife and I have tax free accounts invested in the stock market and I contribute additional investments in my wife's name into a brokerage account for other stock market investments. A mistake I made with this was investing in companies initially some very successful and others not so successful I am not investing in ETF's but across a number of sectors like property, high yield bonds, s&p 500 Euro stocks as I think USA is on a knife edge (just my opinion), gold mining, silver and recently some bitcoin. I agree with you if your young go for the S&P 500 and world etf but as you get closer to retirement bring in some elements of property and precious metals. Your videos are great wish you were around in my early years I have encourages my children to subscribe to your channel it is all the things I wish I had the knowledge to teach them when they were still at home now, they are spread over the world.

Thanks for this Carla. I am assuming that when you calculate your monthly living costs you exclude what you are investing now as by the time you reach this number you will no longer need to keep doing this?